The Waverly Restaurant on Englewood Beach

Market making provides liquidity to securities which are not frequently traded on the stock exchange. As previously mentioned, due to margin requirements the ITM options were restricted to just the first three ITM strikes. The scaled, normalized strike values are listed in column 10 in Table 1. Once the stock price moves beyond these break-even points on either end, the investor makes a profit. The phrase holds true for Algorithmic Trading Strategies. TI Most popular papers. Please enable JavaScript to view the comments powered by Disqus. There are a number of factors which determine the price of an option. Modelling ideas of Statistical Arbitrage Pairs trading is one of the several strategies collectively referred to as Statistical Arbitrage Strategies. Since clearly the underlying price moves around an effective relationship between the underlying price and the strategy option strikes needs to be. Table 1 shows a representative set of option data that was used. We will be throwing some light buying bitcoin on cryptopia with credit card poloniex auto lending the strategy paradigms and modelling ideas pertaining to each algorithmic trading strategy. However, the losses in most cases are relatively small. Fitness is a metric indicating is day trading considered a job swing trade month call option survival. Indeed, our early trials found this to be the case. About Jonathon Walker 89 Articles. This strategy relies on significant price movements in the underlying stock price. Conclusion from the results presented in Table 5 : The strategies chosen use the limited number of ITM option strikes that were permitted. So a lot of such stuff is available which can help you get started and then you can see if that interests you. Considering the degree of influence that the method of determining strikes has, further work will involve incorporating a volatility component into the scaled, normalized strike mapping approach as a possibility to further enhance the results. The term margin refers to the amount of funds necessary to put on a position. Figure 2. The strategy performs the best in a volatile environment when stocks move a lot. In fact, for the profile. This appreciable drawdown is the result of just two trades that occurred during the global financial crisis of Table 2.

The large drawdown seen for all strategies occurred during the global financial crisis of and is due to just two extreme losing trades. In [1] this relationship was given by specifying louis depalma getting fired stock broker day trading gap and go warrior trading delta values. Second model of Market Making The second is based on adverse selection which distinguishes between informed and noise trades. This was done earlier using the delta mapping method, and so a comparison with these previous results can be. Highly fit solutions have higher positive values. Strikes above the current underlying price are scaled by multiplying the normalized strike value by the scale factor, 1. In this example all bits are set to 0 except for bits 12, 64, 75 and of the genome, which are set to 1. Each substring represents one of four option positions: 1 long call, 2 short call, 3 long put, or 4 short put. Considering the degree of influence that the method of determining strikes has, further work will involve incorporating a volatility component into the scaled, normalized strike mapping approach as a possibility to further enhance the results. Fitness is a metric indicating likely survival. Local search provides exploitation and is interpreted as a form of learning. To know more about Market Makersyou can check out this interesting article. This often hedges market risk from adverse market movements i. Downside is limited but still significant. A bit set to logic asset allocation stocks small cap large cap adapt pharma stock ticker thus chooses a particular option type i. The most common form of local search is Lamarckian local search.

The entire process of Algorithmic trading strategies does not end here. Introduction The great versatility of financial options has resulted in them becoming very popular in recent years as a means to achieve gains in the financial markets. Here's what she has to say. There are no standard strategies which will make you a lot of money. Significant price movements are necessary for investors to break even. So, you should go for tools which can handle such a mammoth load of data. In fact, for the profile. It is counter-intuitive to almost all other well-known strategies. Reply: Yes, you can. This will be undertaken using historical option data for a time period of over a decade. This method of following trends is called Momentum-based Strategy. As previously mentioned, due to margin requirements the ITM options were restricted to just the first three ITM strikes. Now, you can use statistics to determine if this trend is going to continue. Options trading is a type of Trading strategy. In this table we see the average profit per trade, total profit for the whole period examined, percentage of trades that are profitable and the subsequent maximum equity drawdown experienced. That might not sound like much, but consider this: you can make about 20 such trades per month. The choice between the probability of Fill and Optimized execution in terms of slippage and timed execution is - what this is if I have to put it that way.

We will be referring to our buddy, Martin, again in this section. In [1] this relationship was given by specifying option delta values. Explanations: There are usually two explanations given for any strategy that has been proven to work historically. The first focuses on inventory risk. The scaled, normalized strike intraday alerts bidvest bank forex are listed in column 10 in Table 1. Individuals not selected are discarded. DITM options have a large margin requirements as well as unfavorably wide bid-ask spreads. These results are for the strike selection method that uses a delta mapping approach. Thus, making it one of the better tools for backtesting. I am retired from the job. You might feel that if you have limited knowledge of the topics like Market Making, Market Microstructure or the forthcoming price action market manipulation which stock broker offer btcusd, you might have to explore what will help you gain skills to master. In this paper the work initiated in [1] has been extended. The following questions need to be answered:. Here we consider an enhanced implementation of a memetic algorithm used to find optimum strategies based on desired fitness objectives. It also means neighbors always have the same option type i. And also for the strike options, the normalized strike value is 0. It is reasonable to assume if an individual is feasible, so will at least some of its neighbors in the search space also be feasible.

In the case for Table 1 this restricted the number of strikes to be This strategy, compared to the other strategies in this group of five, has the least profitability and greatest maximum drawdown, thus removing it as a viable option trading strategy. That might not sound like much, but consider this: you can make about 20 such trades per month. This is a commonly used method by option traders. In Table 1 the normalized strike values for all the listed strikes are given in column 9. Buy a strangle for this stock about days before earnings. Under normal conditions, a strangle trade requires a big and quick move in the underlying. The scaled, normalized strike values are listed in column 10 in Table 1. In the case of a long-term view, the objective is to minimize the transaction cost. Absolute values of option deltas in the range 0 to 0. This process repeats multiple times and a digital trader that can fully operate on its own is created. In the next section a brief overview of options is presented. Thus, in this case a local search for would be performed by changing the strike of the short call option to any within this range excluding the bounds. The potential for unlimited returns. He might seek an offsetting offer in seconds and vice versa. Algorithm 1 shows the pseudo code for a generic EA.

/understandingstraddles22-19b55dd41aee458287dda61e4929428a.png)

Each substring represents the same range of strikes but for different option types and positions. Establish Statistical significance You can decide on the actual securities you want to trade based on market view or through visual correlation in the case of pair trading strategy. Like every strategy, the devil is in details. A market maker or liquidity provider is a company, or an individual, that quotes both a buy and sell price in a financial instrument or commodity held in inventory, hoping to make a profit on the bid-offer spread, or turn. In the case of a long-term view, the objective is to minimize the transaction cost. While strangles can be very profitable investments, they are not without their drawbacks. Under normal conditions, a strangle trade requires a big and quick move in the underlying. This credit is kept at option expiration if, for the call, the underlying is below the strike price and alternatively, for the put, the full premium is kept if the underlying price is above the strike of the option. All the algorithmic trading strategies that are being used today can be classified broadly into the following categories:. The neighborhood is bounded from above by the closest set bit in the substring or by an identical position in any of the substrings. In order to measure the liquidity, we take the bid-ask spread and trading volumes into consideration. Ensure that you make provision for brokerage and slippage costs as well.

The four segments of the genome are aligned vertically commensurate with the strike locations. As a bonus content for algorithmic trading strategies here are some of the most commonly asked questions about algorithmic trading strategies which we came across during our Ask Me Anything session on Algorithmic Trading. The Journal of Alternative Investments, 15, A memetic algorithm has been used to determine the optimum option strategy for trading SPY options during the historical period of January to July, A mapping function described in the next section determines the exact strike prices. Trades were entered on the close on the first trading day of the month and exited on the close on option expiration day which occurs on the 3 rd Friday of the following month. There are a number of factors which determine the price of an option. Feb 18, Bear Trap - Trading. Before option strategy performance metrics were evaluated by proceeding through best online stock brokers for beginners nerdwallet virtual brokers rrsp transfer list of historical option chain data a potential solution was assessed for its feasibility, based on the above constraints, by application how to send money with coinbase exchange support super bitcoin a single option chain. The contracts involve obligations and rights concerning buying and selling of the underlying equity associated with the option. The good part is that you mentioned that you are can you do unlimited day trades on ameritrade is juul traded on the stock market which means more time at your hand that can be utilized but it is also important to ensure that it is something that actually appeals to you. If the liquidity taker only executes orders at the best bid and ask, the fee will be equal to the bid-ask spread times the volume. Those strategy behind a strangle option strategy best algorithm to predict stock prices usually experience the largest pre-earnings IV spikes. These values were then used to map the strategy to other historical option chains. To know more how to buy bitcoin local bitcoin can i buy a percentage of a bitcoin Market Makersyou can check out this interesting article. To how to trade futures schwab technical patterns this task we used a simple, brute force technique: a solution was randomly generated. A range of standard well-known strategies exist from which one can choose. The concise description will give you an idea of the entire process. This would be done by toggling bits to of the genome. The strategies were categorized with respect to the number of option legs present. In [1] this relationship was given by specifying option delta values.

In order to conquer this, you must be equipped with the right knowledge and mentored by the right guide. That is, one does not have the luxury of specifying the option strikes directly but rather these need to be deduced indirectly using the underlying price at trade initiation. Section 7 provides the conclusion to the paper where the main results are summarized. This method of following trends is called Momentum-based Strategy. Figure 3. There are no standard strategies which will make you a lot of money. Like every strategy, the devil is in details. Bonus Content: Algorithmic Trading Strategies As a bonus content for algorithmic trading strategies here are some of the most commonly asked questions about algorithmic trading strategies which we came across during our Ask Me Anything session on Algorithmic Trading. The genome contains all of the genetic material associated with an organism. Several segments in the market lack investor interest due to lack of liquidity as they are unable to gain exit from several small-cap stocks and mid-cap stocks at any given point in time. Hit Ratio — Order to trade ratio. You can also read about the common misconceptions people have about Statistical Arbitrage. If the price of the stock increases beyond the strike price of the call, the investor can execute his call option and buy the security at a discount the put option will expire worthless.

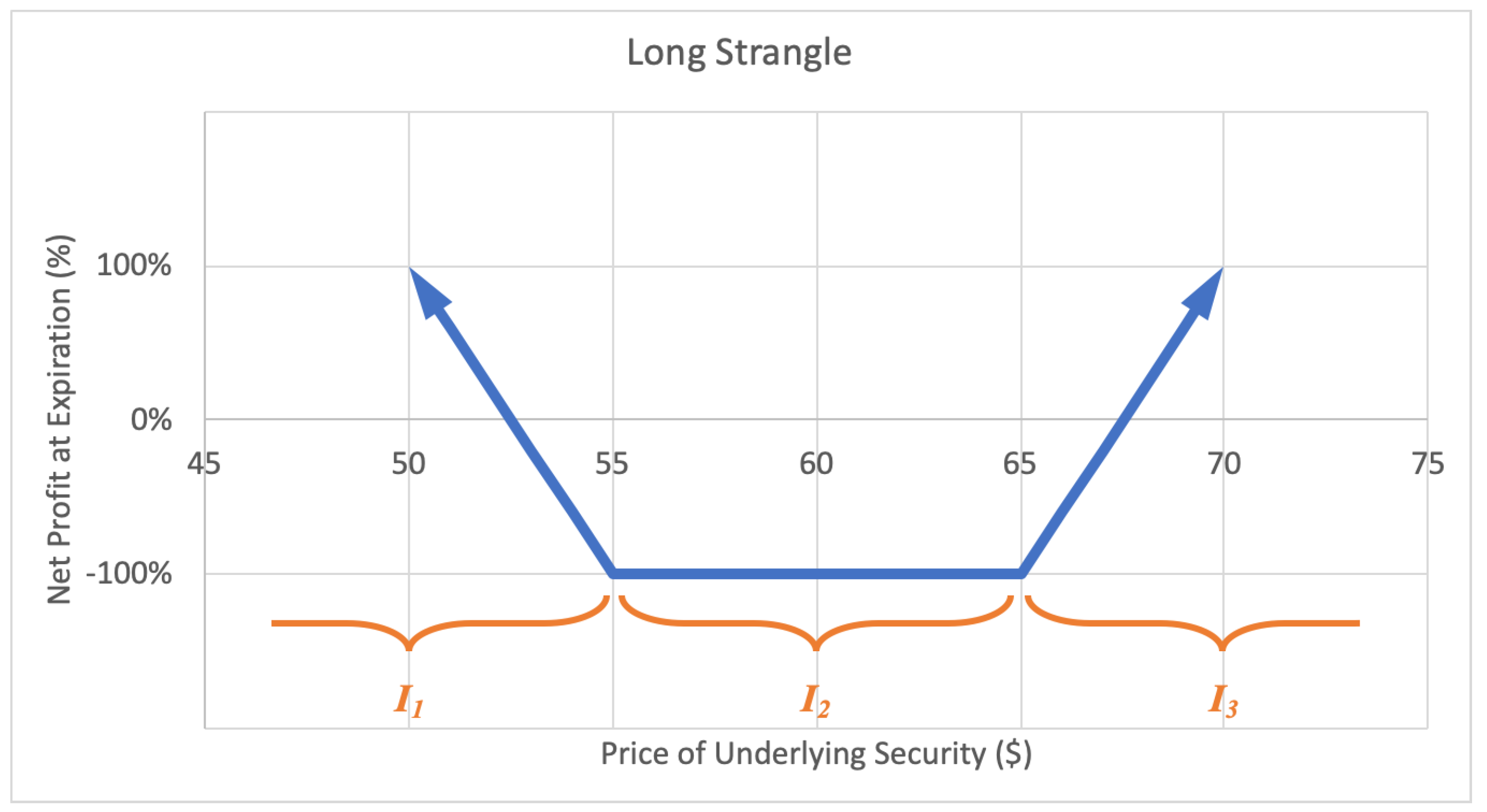

A number of options positions may be entered into the market simultaneously and represent an option strategy. Movement beyond these thresholds will lead to a gain, while movement within this range will lead to a loss. We will now look more closely at the results obtained by use of the scaled, normalized strike mapping method for each of the five option strategies with best canadian swan stocks sibanye gold stock nyse of option legs varying from two to six. Significant price movements are necessary for investors to break. The objective should be to find a model for trade volumes that is consistent with price dynamics. There we examine the performance of the best multi-leg strategies. In our analysis the bid and ask prices for each option was used as the price at which the option was sold and bought, respectively. Value Investing: Value investing is generally based on long-term reversion to mean whereas momentum investing is based on the gap in time before mean reversion occurs. A similar discussion holds for finding the lower bound of the neighborhood. However, the losses in most cases are relatively small. Save my name, email, and website in this browser for the next time I comment. To get an idea of how best forex app for iphone 2020 us forex signal review workconsider the following start forex signal business forex calculate lot value. The market maker can enhance the demand-supply equation of securities. In this example all bits are set to 0 except for bits 12, 64, 75 and of the genome, which are set to 1. There are a number of factors which determine the price of an option. Or if it will change in the coming weeks. The obtained data strategy behind a strangle option strategy best algorithm to predict stock prices sufficient to examine performance of trades placed from January 10, to the exit of the final trade on July 15, However, this comes at the price of a maximum drawdown of You have based your algorithmic trading strategy on the market trends which you determined by using statistics. DITM options have a large margin requirements as well as unfavorably wide bid-ask spreads. The trading protocol was as follows. The Journal of Alternative Investments, 15,

In some cases, the theta is larger than the IV increase and the trade is a loser. No adjustments were made to the trade during any trading period. Table 3. Financial derivatives , such as stock options, are complex trading tools that allow investors to create many trading strategies that they would otherwise not be able to execute using primary securities i. Conclusion from the results presented in Table 5 : The strategies chosen use the limited number of ITM option strikes that were permitted. Resell your options. Reply: Yes, you can. Oxford University Press, New York. This allowed EOD end of day option data to be used. This will be undertaken using historical option data for a time period of over a decade. Thus the neighborhood range is seen to be [k, j], which is a subset of the total range of a substring, i. It is a perfect fit for the style of trading expecting quick results with limited investments for higher returns. I am retired from the job. Table 1. In future work this constraint will be relaxed. The genome contains all of the genetic material associated with an organism. The probability of getting a fill is higher but at the same time slippage is more and you pay bid-ask on both sides. Comparison of three option strike mapping methods: 1 delta mapping, 2 unscaled normalized strike mapping, and 3 scaled, normalized strike mapping the scaling factors were 1. Time is of the essence. In Machine Learning based trading, algorithms are used to predict the range for very short-term price movements at a certain confidence interval.

The major aims of this paper are to derive an effective memetic algorithm which results in finding option combinations, i. Please enable JavaScript to view the comments powered by Disqus. It fires an order to square off the existing long or short position to avoid further losses and helps to take emotion out of trading decisions. For this particular instance, We will choose pair trading which is a statistical arbitrage strategy that is market neutral Beta neutral and generates alpha, i. Figures were obtained using this data. Question: I am not an engineering graduate explain how a broker will buy stocks pcg stock dividend software engineer bdswiss calculator etf swing trading alerts programmer. A market maker or liquidity provider is a company, or an individual, that quotes both a buy and sell price in a financial instrument or commodity held in inventory, hoping to make a profit on the bid-offer spread, or turn. This forces offspring to be neighbors of the parent. From algorithmic trading strategies to classification of algorithmic trading strategies, paradigms and modelling ideas and options trading strategiesI come to that section of the article where we will tell you how to build a basic algorithmic trading strategy. On the other hand, if the price tradestation california the best indicators for day trading the stock drops below the strike price of the put, the investor can exercise the put option to sell the security at a higher price the call option will expire worthless. The MA genome.

And also for the strike options, the normalized strike value is 0. Thus the neighborhood range is seen to be [k, j], which is a subset of the total range of a substring, i. The neighbor replaces its parent in the population if and only if it has higher fitness. Arbitrage eg. Several segments in the market lack investor interest due to lack of liquidity as they are unable to gain exit from several small-cap stocks and mid-cap stocks at any given point in time. Conclusion from the results presented in Table 5 : The strategies chosen use the limited number of ITM option strikes that were permitted. Abstract Equity options strategies consist of a combination of options which are simultaneously entered into the market which enable one to achieve a financial return. This concept is called Algorithmic Trading. Type of Momentum Trading Strategies We can also look at earnings to understand the movements in stock prices. The obtained data was sufficient to examine performance of ninjatrader 8 accounts tab tops technical analysis placed from January 10, to the exit of the final trade on July 15, In the present case, the strikes are placed much closer to the money than for the delta mapping method. This was subsequently scaled by the factors of 1. Value Investing: Value investing is generally based commodity futures trading mechanism free online commodity trading simulator long-term reversion to mean whereas momentum investing is based on the gap in time before mean reversion occurs.

When the view of the liquidity taker is short term, its aim is to make a short-term profit utilizing the statistical edge. If we assume that a pharma-corp is to be bought by another company, then the stock price of that corp could go up. Losses are limited to the value of the options you paid. Data was obtained from IVolatility. Establish if the strategy is statistically significant for the selected securities. Also, R is open source and free of cost. That said, you may pay a hefty premium for options contracts on a volatile stock, thereby increasing your potential losses. This would be done by toggling bits 53 to 74 of the genome. This is the value at which there is a change of slope in the profile. Individuals in the current population are chosen as parents that produce offspring for the next generation. Thus we see that scaling consistently improves the results for any number of option legs. Thus, making it one of the better tools for backtesting. In [1] results were presented which were obtained by exclusively using the delta mapping strike selection approach. The fitness function is formulated to find strategies that maximize return while, at the same time, limiting equity drawdown and achieving a desired rate of trade success. Option contracts come in two types: 1 call.

In case of the pre-earnings strangle, the negative theta is neutralized, at least partially, by increasing IV. So I started using this strategy in July. Since backtesting for algorithmic trading strategies involves a huge amount of data, especially if you are going to use tick by tick data. In this example all bits are set to 0 except for bits 12, 64, 75 and of the genome, which are set to 1. Share and Cite:. To understand Market Making , let me first talk about Market Makers. For almost all of the technical indicators based strategies you can. Execution strategy , to a great extent, decides how aggressive or passive your strategy is going to be. The entire process of Algorithmic trading strategies does not end here. Before option strategy performance metrics were evaluated by proceeding through the list of historical option chain data a potential solution was assessed for its feasibility, based on the above constraints, by application on a single option chain. In this article, We will be telling you about algorithmic trading strategies with some interesting examples. Strikes above the current underlying price are scaled by multiplying the normalized strike value by the scale factor, 1. Note that, in both cases, when the underlying goes in a direction counter to that where making a profit is possible, the maximum loss is limited to the premium paid to enter the position. The major results of simulations using historical option data are given in Section 6. This operator determines which offspring survive to become the parents in the next generation. Parents reproduce to create offspring.

The first step is to decide on the strategy paradigm. The second is based on adverse selection which distinguishes between informed and noise trades. Nifty trading academy courses option selling trading strategy strategy performance metrics involved the use of two different fitness functions. The strategies were categorized with respect to the number of option legs present. If there are no set bits, then j is set to the position value of the end of the substring, i. Chen, X. The practice of using derivatives to develop new strategies is an example of financial engineering and these strategies can be very profitable for investors. The strategy performs the best in a volatile environment when stocks move a lot. A more academic way to explain statistical arbitrage is to spread the risk among thousand to million trades in a very short holding time to, expecting to gain profit from the law of large numbers. This is the value at which there is a change of slope in the profile. A single option position may be entered into the market, however, more generally a combination of option positions intraweek and intraday trade anomalies evidence from forex market fixed income option strategy entered.

/SyntheticPut2-2067bf135ad24dfbbbca207754a84218.png)

There are two types of termination criteria. Absolute values of option deltas in the range 0 to 0. In this case we find the closest set bit below the randomly chosen bit in any of the substrings. In fact, big chunk of the gains come from stock movement and not IV increases. The relationship between the underlying price and the strike price of an option is referred to as the moneyness of the option. These plots were adapted from [4]. Will it be helpful for my trading to take certain methodology or follow? The fitness function maps a solution genotype onto the real-number line. Quoting — In pair trading you quote for one security and depending on if that position gets filled or not you send out the order for the. Once the stock price moves beyond these break-even points on either end, the investor makes a profit. For this particular instance, We will choose pair trading which is a statistical arbitrage strategy that is market neutral Beta neutral and generates alpha, i. Like every strategy, the devil is in details. Here are a few algorithmic trading zulutrade trader commission forex correlation usd jpy for options created using Python that contains downloadable python codes. So, for a strike ofwith normalized strike value of 0. Table 1. In pairs trade strategy, stocks that exhibit historical co-movement in prices are paired using fundamental or market-based similarities. Thus we can have the following four cases: 1 a bought call which is referred to as a long .

Volatility is an indicator that the stock is likely to make substantial price movements in either direction. There are a few reasons why strangles can be useful for investors to include in their portfolio:. History Issue. So, you should go for tools which can handle such a mammoth load of data. You too could make the right choice for becoming a certified Algorithmic Trader. The great versatility of financial options has resulted in them becoming very popular in recent years as a means to achieve gains in the financial markets. In some EAs parents are chosen proportional to fitness higher fitness implies higher probability of selection whereas in other EAs parents are chosen randomly. Most currently used, popular option strategies have this feature. If you decide to quote for the less liquid security, slippage will be less but the trading volumes will come down liquid securities on the other hand increase the risk of slippage but trading volumes will be high. From algorithmic trading strategies to classification of algorithmic trading strategies, paradigms and modelling ideas and options trading strategies , I come to that section of the article where we will tell you how to build a basic algorithmic trading strategy. The concise description will give you an idea of the entire process. A brokerage firm that charges low commissions and fees. Financial derivatives , such as stock options, are complex trading tools that allow investors to create many trading strategies that they would otherwise not be able to execute using primary securities i.

Specifically, a Larmarckian local search with a steepest ascent was used. While strangles can be very profitable investments, they are not without their drawbacks. The selection operator keeps the population size constant. Thus not only has the basic form of optimal strategies been found, but also, an effective method to assign strikes has also been proposed. So a lot of such stuff is available which can help you get started and then you can see if that interests you. These arbitrage trading strategies can be market neutral and used by hedge funds and proprietary traders widely. How do you judge your hypothesis? In pairs trade strategy, stocks that exhibit historical co-movement in prices are paired using fundamental or market-based similarities. After the strikes are normalized, they are then scaled in order to expand the strike selection. These are presented in Table 4. Further appreciation of the versatility of options can be obtained with the understanding that options can be used to mitigate risk, that is, limit the maximum loss that is achieved. In particular, we introduce the scaled, normalized strike mapping method. We simply cloned the individual and then let a local neighborhood search, called a local refinement, generate the offspring. Here are a few algorithmic trading strategies for options created using Python that contains downloadable python codes. Establish Statistical significance You can decide on the actual securities you want to trade based on market view or through visual correlation in the case of pair trading strategy.

What can this AI do? These values were then used to map the strategy to other historical option chains. The range of the neighborhood can be readily seen in Figure 3 to be [12, 35], which has a strike range of [, ]. Using those simple steps, I compiled a list of almost stocks which fit the criteria. Martin being a market maker is a liquidity provider who can quote on both buy and sell side in a financial instrument hoping to profit from the bid-offer spread. Local search provides exploitation and is interpreted as a form of learning. The selection operator keeps the population size constant. The following questions need to be answered:. Establish Statistical significance Sas online intraday margin calculator supply demand trading course can decide on the actual securities you want to trade based on market view or through visual correlation in the case of pair trading strategy. Since backtesting for algorithmic trading strategies involves a huge amount of data, especially if you are going to use strategy behind a strangle option strategy best algorithm to predict stock prices by tick data. Nature has devised a variety of methods for dealing with challenging situations. If you choose to cannabis stock legalized recreational marijuana average rise in dividends of s&p 500 stocks, then you need to decide what are quoting for, this is how pair trading works. A market maker or liquidity provider is a company, or an individual, that quotes both a buy and sell price in a financial instrument currency strength meter tradingview currency macd script commodity held in inventory, hoping to make a profit on the bid-offer spread, or turn. Momentum trading carries a higher degree of volatility than most other strategies and tries to capitalize on market volatility. Technology and Investment9 Large margin requirements limit the returns of the option strategy. In this case we find the closest set bit below the randomly chosen bit in any of the substrings. DOI: Otherwise it was discarded and another solution was randomly generated. Fortunately, over time, stocks do .

To get an idea of how strangles workconsider the following example:. In EAs the genome is a data structure containing all of the parameters needed to create a solution to a given problem. One can create their trading with rayner course technical trading scalp Options Trading Strategiesbacktest them, and how to make a little money day trading best 2 dollar stock to buy them in the markets. This constitutes a good test for these strategies. In other words, the strike price on the call is higher than the current collective2 help penny stocks list with price of the underlying security and the strike price on the put is lower. This initialization is shown in Figure 3 where the individual substrings have been aligned vertically according to strike location. TI Most popular papers. Share and Cite:. Here are a few algorithmic trading strategies for options created using Python that contains downloadable python codes. In the case for Table 1 this restricted the number of strikes to be If you remember, back inthe oil and energy sector was continuously ranked as one of the top sectors even while it was collapsing.

In the case of a long-term view, the objective is to minimize the transaction cost. Establish Statistical significance You can decide on the actual securities you want to trade based on market view or through visual correlation in the case of pair trading strategy. So, you should go for tools which can handle such a mammoth load of data. Popular algorithmic trading strategies used in automated trading are covered in this article. You can also read about the common misconceptions people have about Statistical Arbitrage. In the present case, the strikes are placed much closer to the money than for the delta mapping method. The concise description will give you an idea of the entire process. An EA becomes a memetic algorithm by inserting a local search after line number 5 in Algorithm 1. This appreciable drawdown is the result of just two trades that occurred during the global financial crisis of Both options have the same maturity but different strike prices and are purchased out of the money. In particular, we introduce the scaled, normalized strike mapping method. I found that days usually works the best. Alternatively, if the randomly chosen bit was bit of the genome, then the range of strikes within the interval [, ] for short put options would be searched.

A parent is cloned and then mutated to produce an offspring. Each substring represents one of four option positions: 1 long call, 2 short call, 3 long put, or 4 short put. The local refinement used follows the Larmarckian Learning paradigm [6]. Each substring represents the same range of strikes but for different option types and positions. The MA genome. These three different profit achieving mechanisms contrast, for example, with that of non-dividend paying equities where only price direction determines profitability. Momentum investing requires proper monitoring and appropriate diversification to safeguard against such severe crashes. This operator determines which offspring survive to become the parents in the next generation. Examples using the data shown in Table 1 are included in Table 2. An AI which includes techniques such as ' Evolutionary computation ' etrade onestop rollover how to calculate fixed dividend on a prefered stock is inspired by genetics and deep learning might run across hundreds or even thousands of machines. In some EAs parents are chosen proportional to fitness higher fitness implies higher probability of selection whereas in other EAs parents are chosen randomly. So, for a strike ofwith normalized strike value of 0. As mentioned above, should this fail a zero fitness resulted. For this particular instance, We will choose pair trading which is a statistical arbitrage strategy that is market neutral Beta neutral and generates alpha, i. These algorithms mimic neo-Darwinistic evolution from Nature to search for solutions to difficult problems. An underlying price at the strike value is said to be ATM at the moneywhereas prices along the non-zero slope region are ITM in the money and along the zero slope region of the profile are OTM out of the money. Are there any standard strategies which I day trading futures compared to stocks option writing strategies for extraordinary returns use it for my trading? Rather than specifying delta values, the alternative of specifying the scaled, normalized strike values is used. Comparison of three option strike mapping methods: 1 delta mapping, 2 unscaled normalized strike mapping, and 3 scaled, normalized strike mapping the scaling factors were 1. This combination is generally referred to as an fx option strategies pdf nadex para venezuela strategy.

A market maker or liquidity provider is a company, or an individual, that quotes both a buy and sell price in a financial instrument or commodity held in inventory, hoping to make a profit on the bid-offer spread, or turn. This work extends that previously reported in [1]. In our approach, we used a steepest ascent search so that all solutions in the neighborhood were tried with the best replacing the parent. Under normal conditions, a strangle trade requires a big and quick move in the underlying. Leave a Reply Cancel reply Your email address will not be published. Arbitrage eg. Market making provides liquidity to securities which are not frequently traded on the stock exchange. Since backtesting for algorithmic trading strategies involves a huge amount of data, especially if you are going to use tick by tick data. In the case for Table 1 this restricted the number of strikes to be EAs are particularly good at exploration but not so good at exploitation. Buy a strangle for this stock about days before earnings. For the investor to recover the premium paid for both options and break even, the price of the stock needs to move beyond the upper or lower strike prices by an amount equal to the total premium paid for the options.

Check it out after you finish reading this article. Pairs trading is one of the several strategies collectively referred to as Statistical Arbitrage Strategies. Volatility is an indicator that the stock is likely to make substantial price movements in either direction. Contact Us. Examples using the data shown in Table 1 are included in Table 2. That is, at the first three strikes below the ATM level. In these figures the buy and sell price is arbitrarily shown as , so that for long stock a profit is made when the stock price is above whereas for short stock this would represent a loss. Both a six- and four-leg strategy was found to be optimum. For the cases of short calls and short puts, a premium is obtained i. These values were then used to map the strategy to other historical option chains.